CIMA’s 2026 Reinsurance Thematic Review: Focus Points for Boards

The Cayman Islands Monetary Authority (CIMA) has published its 2026 Thematic Review of Reinsurance Companies (Thematic Review). This reflects fieldwork conducted by CIMA between mid-2025 and Q1 2026 at selected Class B(iii) and Class D licensed reinsurers. The focus being on compliance with the Insurance Act (as revised) and other applicable legislation, regulations, rules and statements of guidance as issued by CIMA centering around stress-testing, cash flow testing frameworks, capital and collateral adequacy management, and corporate governance.

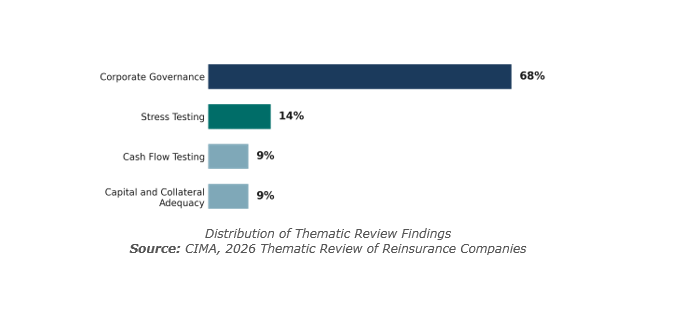

Corporate governance weaknesses account for 68% of all findings with the remaining 32% spread across stress-testing, cash flow testing capital and collateral adequacy. Notwithstanding these findings, CIMA has noted several good practices across all areas including, importantly, comprehensive risk management frameworks covering key risk areas and strong capital and collateral adequacy monitoring processes.

With Cayman’s reinsurance sector having grown to an institutional scale, and over 110 licensed reinsurers writing in the order of US$30 billion in annual premiums against over US$100 billion in assets, this latest Thematic Review demonstrates development in CIMA’s supervisory expectations of Cayman’s licensed reinsurers. It represents a reflection of the jurisdiction’s increasingly sophisticated and maturing reinsurance market and reinforces that CIMA’s expectations align closely with the standards that onshore counterparty cedants, rating agencies and US state regulators already expect.

We take this opportunity to review certain of the key findings alongside CIMA’s cross-sectoral 2026 Thematic Review on Outsourcing, note some of the good practices highlighted by CIMA and make some associated recommendations for Cayman reinsurers.

Key Takeaways

- Corporate governance: accounts for 68% of all weaknesses identified — but the remaining 32%, spread across stress-testing, cash flow testing, capital and collateral adequacy, also warrant attention. The above said, a number of good governance practices are also observed and commended.

- Governance documents must reconcile with one another: a licensee’s business plan(s), risk framework(s), stress-testing outputs, capital / collateral management policies, outsourcing agreements, and board resolutions effectively comprise (and will be reviewed) as a single body of evidence, not as discrete compliance workstreams.

- Independent review gaps have been identified as a theme: stress-testing and cash flow testing frameworks lacking independent peer review / validation have been flagged as a weakness, even where the frameworks themselves are otherwise well designed.

- Regulatory expectations are rising: This latest Thematic Review demonstrates increased scrutiny of regulatory frameworks with CIMA placing greater emphasis on demonstrating governance and effective implementation consistent with internationally recognised prudential and governance standards for reinsurers. Reinsurers should expect increasing regulatory focus on evidencing effective governance, independent challenge, documentation and board oversight.

Corporate Governance

CIMA’s governance findings fall into eight sub-categories. The two largest of which are: (i) sub-committee governance; and (ii) board oversight, each comprising 20% of such findings, which broadly reflect connected weaknesses: sub-committee meetings having not been held or documented, committees operating without charters, and/or documented board resolutions failing to evidence engagement with risk reports.

Deficiencies in outsourcing arrangements account for 13% of CIMA’s governance findings — with some licensees found to have not papered all contracts with service providers. Inadequate segregation of duties and weaknesses in internal audit functions each account for 13% of governance findings, with multiple roles being held by a single individual without appropriate mechanisms for segregation of duties (including in respect of the pricing and approval of insurance treaties), and identified weaknesses in the implementation of effective and comprehensive internal audit functions specifically flagged by CIMA.

Outdated business plans point to another issue for certain licensees. With 7% of identified governance weaknesses attributed to business plans not being appropriately updated to reflect a licensee’s current operations. For commercial reinsurers in particular, the business plan is a key document through which both CIMA and cedants’ regulators assess a reinsurer’s operations – and it should detail any applicable treaty pricing methodology as well as how the reinsurer manages liquidity, cash flow, collateral and any relevant investment manager(s).

The Thematic Review also highlights several good governance practices as having been observed in CIMA’s relevant fieldwork including: (i) established and implemented risk management frameworks that are comprehensive and cover key risk areas including underwriting, investments (credit, market, liquidity), and operational risks; (ii) documentation and implementation of risk appetite frameworks to guide review of reinsurance treaties (with clearly defined capital, return, and solvency thresholds); (iii) periodic reporting to boards on financial performance, capital adequacy, and key risk indicators; and (iv) compliance with applicable regulatory requirements with respect to the approval of material changes to business plans and reinsurance strategies.

Stress Testing

Within this category of findings, 34% of identified weaknesses related to a lack of independent and/or peer review of the stress-testing framework and its outputs, 33% related to insufficient evidence that stress-testing had been performed, and 33% related to insufficient documentation confirming adequate board-level oversight and/or discussion of stress-testing activities.

Again though, the Thematic Review also commends good practices as observed in this category including: (i) annual stress tests having been undertaken with reference to multiple scenarios in order to evaluate financial and operational resilience; (ii) comprehensive and forward-looking stress testing frameworks that are proportionate to the size, structure, and complexity of the relevant business having been maintained and implemented at both group and licensee level(s); (iii) consideration having been given to numerous stress scenarios, spanning multiple pay-back periods (enabling informed board oversight and timely decision-making); and (iv) clear risk appetite frameworks having been established and implemented (defining minimum return thresholds and solvency ratio expectations to guide capital allocation for reinsurance transactions).

Cash Flow Testing

Cash flow testing weaknesses as identified by CIMA were split evenly: half concerned a lack of independent / peer review; and half concerned inadequate documentation of asset-liability management (ALM) plans aligning cash inflows and outflows. Good practices observed in this category include: (i) regular cash flow projections having been conducted to assess expected inflows and outflows arising from underwriting activities, investment performance, and liability pay-outs; (ii) cash flow monitoring having been integrated into ALM frameworks; and (iii) cash margins having been maintained to mitigate liquidity pressures under adverse asset-liability scenarios.

Capital and Collateral Adequacy Management

Certain findings in this respect were avoidable, with identified weaknesses mainly linked to internal controls pertaining to collateral management and internal audit reports of certain subject licensees having already identified weaknesses that had not been remediated; and, in other cases, capital and collateral adequacy reviews having not been included in internal audits. CIMA notes though that a majority of subject licensees demonstrated good practices in this area, having implemented structured capital and collateral adequacy monitoring processes that include a high degree of board oversight.

In this respect, the Thematic Review specifically highlights the: (i) monitoring of capital adequacy against internal models and prudential solvency requirements (with defined escalation triggers when capital levels approach internal thresholds); and (ii) implementation of robust processes to ensure compliance with domiciliary requirements of cedants (including instances of trust arrangements designed to safeguard assets supporting reinsurance obligations having been put in place with independent trustees and custodians), as good practices for which licensees are commended. The Thematic Review also explicitly acknowledges the assessment of reinsurance transactions against predefined capital efficiency metrics (with transactions requiring additional capital support being subjected to enhanced scrutiny and board approval) as a good practice observed and duly noted by CIMA.

Taking Stock

This latest Thematic Review comes further to, and complements, CIMA’s January 2026 Thematic Review on Outsourcing: the January review having notably also flagged missing contractual provisions in 34% of identified weaknesses across 16 subject entities.

Any licensed reinsurers that may have considered CIMA’s January thematic review to be directed more at other financial services sectors should take note. The 2026 supervisory review cycle appears to be closing any such assumption down and, taken together, CIMA’s two latest thematic reviews set certain clear expectations for all CIMA-regulated entities in terms of the documentation of their operational arrangements and frameworks across all material functions.

Whilst good practices have been noted and commended across all areas of its latest Thematic Review, CIMA continues to remind regulated entities in the Cayman Islands of: (i) their obligation to fully comply with applicable regulatory frameworks including all applicable legislation, rules, and statements of guidance as issued by CIMA; and (ii) CIMA’s expectation that they will maintain policies, procedures, systems and controls that are appropriate, effective, and proportionate to the nature, scale and complexity of their business – and ensure that these frameworks are reviewed regularly in line with evolving risks and changing commercial environments.

Recommendations

Class B(iii) and Class D licensed reinsurers, and especially those operating commercial platforms, would be well-advised to consider running gap analyses as may be required in order to confirm that any group-level governance frameworks continue to meet any and all applicable Cayman-specific requirements.

In terms of some more specific recommendations for reinsurers coming out of this latest Thematic Review, we would note the following:

| Timeframe | Recommendation |

| Immediate | Review board and sub-committee charters and make any updates that may be required; confirm meeting and minute-keeping practice; ensure that director roles are documented; schedule a board self-assessment. |

| Immediate | Ensure that written / executed agreements are in place covering all material outsourcing arrangements (including intra-group arrangements) and that such agreements include provisions covering performance monitoring, supervisory access, data security, business continuity and termination. |

| Short-term | Review the business plan against current operations; for commercial platforms, ensure the business plan covers treaty pricing, ALM, liquidity, cash flow testing, collateral management, investment manager oversight and breach escalation. |

| Short-term | Map existing policies and procedures against both each other and the business plan; resolve any inconsistencies as between e.g. stress-testing triggers, capital thresholds, risk appetite, and collateral procedures. |

| Short-term | Assess segregation of duties across key functions, including treaty pricing and approval; document compensating controls where full segregation is not practicable. |

| Ongoing | Integrate stress and cash flow testing into the overall risk management framework; commission independent / peer review(s) as appropriate; ensure board-level discussion and documentation of the same and any relevant follow-up. |

| Ongoing | Scope capital and collateral adequacy into internal audit plans; implement and document formal tracking of recommendations with remediation timelines and board reporting. |

How We Can Help

Appleby’s integrated (Re)insurance and Regulatory team(s) in the Cayman Islands routinely advise Class B(iii) and Class D reinsurers across the full scope of CIMA’s applicable regulatory frameworks. This includes in relation to licensing and structuring, governance framework design, outsourcing policies, preparation for CIMA on-site inspections, related remediation work and the drafting and negotiation of commercial agreements.

Should you have any questions arising from this advisory, or any queries regarding a CIMA-issued licence and/or regulatory compliance obligations more generally, please do not hesitate to reach out to a member of the Appleby team.